Washington Post: ‘A way of monetizing poor people’: How private equity firms make money offering loans to cash-strapped Americans

July 3, 2018

Earlier this week, the Washington Postpublished a long investigative piece on private equity firm Warburg Pincus’ investment in Mariner Finance, a subprime installment lender:

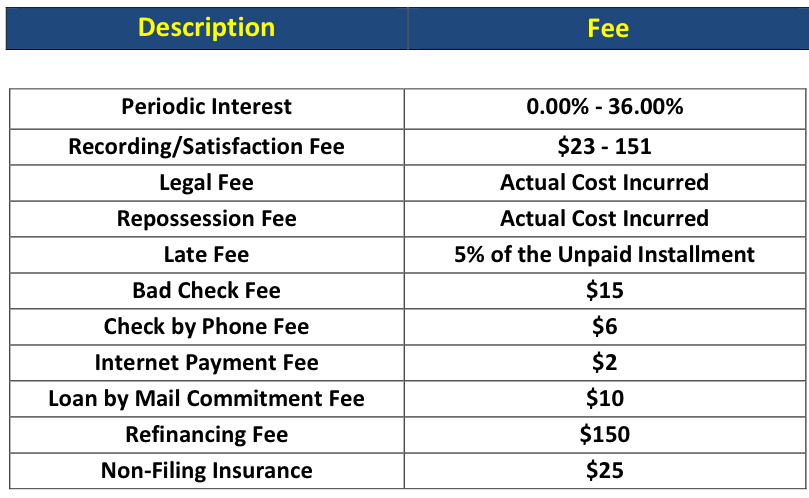

“Mass-mailing checks to strangers might seem like risky business, but Mariner Finance occupies a fertile niche in the U.S. economy. The company enables some of the nation’s wealthiest investors and investment funds to make money offering high-interest loans to cash-strapped Americans.

Mariner Finance is owned and managed by a $11.2 billion private equity fund controlled by Warburg Pincus, a storied New York firm. The president of Warburg Pincus is Timothy F. Geithner, who, as treasury secretary in the Obama administration, condemned predatory lenders. The firm’s co-chief executives, Charles R. Kaye and Joseph P. Landy, are established figures in New York’s financial world. The minimum investment in the fund is $20 million.”

Warburg Pincus’ Mariner Finance is one of several payday lenders and subprime installment lenders acquired by private equity firms over the past several years. Earlier this year private equity giant Apollo announced it was buying OneMain Financial (formerly Springleaf Financial) the largest subprime installment lender. JLL Partners, another private equity firm, owns ACE Cash Express, the second largest payday lender in the US, which charges up to 890% interest on loans.

In December, Americans for Financial Reform, the Center for Responsible Lending, the National Consumer Law Center and People’s Action sent letters to private equity firms invested in payday and subprime installment lenders asking them to agree to basic standards to protect consumers.

More information available in the report from AFR and the Private Equity Stakeholder Project.