Broken Promises: Regulators Question Leonard Green’s Investment in Prospect Medical Holdings

July 31, 2020

Leonard Green & Partners owns Prospect Medical Holdings, a safety net hospital chain that operates seventeen hospitals in five states. Over the course of their ownership, Leonard Green and other owners have collected at least $658 million in fees and dividends from Prospect despite operating challenges, substantially underfunded pensions, and regulatory scrutiny.[1]

Now, Leonard Green is attempting to sell its majority stake in Prospect to the company’s management for $10 million.[2]

In 2014, Prospect acquired Roger Williams Medical Center and Our Lady of Fatima Hospital in Rhode Island, converting them from non-profit to for-profit hospitals.[3] Prospect’s financial statements and disclosures it has submitted to regulatory agencies in Rhode Island raise questions about Prospect’s adherence to commitments to state regulators and accounting practices.

“Overall, questions still remain about the purchase price for the Proposed Transaction and payments of dividends in recent years.”

Rhode Island Office of the Attorney General and Department of Health, July 14, 2020

The Rhode Island Office of the Attorney General and the Department of Health, which are the state’s reviewing authorities for hospital transactions, have extended their timeline to review and approve Leonard Green’s proposed exit. In a letter to Prospect they wrote that, “Overall, questions still remain about the purchase price for the Proposed Transaction and payments of dividends in recent years.”[4]

Key Points:

- The Leonard Green & Partners-led ownership group collected at least $658 million in fees and dividends from Prospect.

- A $457 million debt-financed dividend was paid in 2018 after Prospect represented to the Rhode Island Attorney General and Department of Health that it would not pay more dividends for the forseeable future.

- The 2018 dividend may have pushed Prospect into technical insolvency.

- As a condition of purchasing the CharterCARE hospitals, Prospect committed to making at least $61 million in long term capital contributions to the hospitals. As of the deadline in June 2020, the independent monitor for the Rhode Island Attorney General could only confirm less than half of the required expenditures.

- Several of Prospect’s claims about how it sought to fulfill its capital commitments in Rhode Island are misleading, including an attempt to count $14.4 million in operating losses from its physicians’ practices and unpaid management fees from the hospitals as capital expenditures.

- Prospect received tax breaks in Providence and North Providence based on the understanding that it would fulfill the long-term capital commitment.

- Contrary to representations made by Prospect and Leonard Green, the sale-leaseback of almost all of Prospect’s real estate left the company in a worse financial position than before the transaction.

Dividends

According to Prospect’s annual financial statements, the Leonard Green-led ownership group has collected at least $658 million in dividends from Prospect over the course of its ownership.[5]

Fees and Dividends paid to Leonard Green and other Prospect owners

| Type | Date | Amount |

| Annual $1 Mil Management Fee[6] | 2011-2019 | $9,000,000 |

| Ivy Holdings Merger Transaction Fee[7] | 2010 | $4,441,000 |

| Dividend | 2012 | $88,000,000 |

| Dividend | 2013 | $100,000,000 |

| Dividend | 2018 | $457,000,000 |

| Total[i] | $658,441,000 |

Sources: Prospect Medical Holdings, Inc. Consolidated Annual Financial Statements.[8]

The owners collected the largest dividend after representing to the Rhode Island Attorney General and Department of Health that Prospect would not pay any more dividends. The Attorney General’s decision to approve the hospitals’ conversion from non-profit to for-profit entities states:

“Prospect’s management and representatives have given assurances that this was a one-time event and that there are no plans to make a similar distribution in the foreseeable future.”[9]

At the same time, the Rhode Island Department of Health noted,

“PMH [Prospect Medical Holdings] has represented that there are no intentions to make additional distributions.”[10]

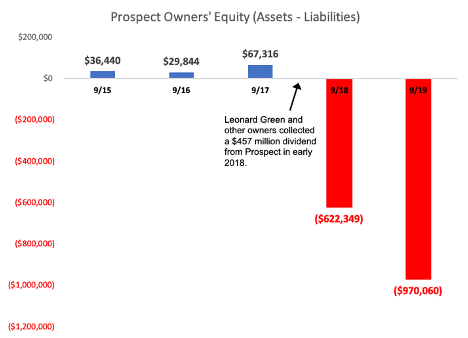

Prospect paid a $457 million dividend to its ownership group in 2018, just four years later, even as its financial performance was declining. Prospect generated a $244 million net loss in 2018.[11]

As a result of the 2018 dividend to Leonard Green and other owners, the safety net hospital chains ran out of cash by early 2019. Ratings agency Moody’s noted that “Prospect exited its first quarter ending December 31, 2018 without any unrestricted cash and $20 million of availability on its ABL facility,” forcing the owners to provide a $41 million cash infusion.[12]

2018 Dividend May Have Pushed Prospect Medical Holdings into Technical Insolvency

The 2018 dividend may have pushed Prospect into technical insolvency, wherein its liabilities are greater than its assets.

As of September 2017, prior to the dividend, Prospect Medical Holdings reported $1.818 billion in assets and $1.795 billion in liabilities. A year later however, following the dividend, Prospect’s liabilities ($2.440 billion) were substantially greater than its assets ($1.862 billion), suggesting that the 2018 dividend may have rendered Prospect Medical Holdings technically insolvent.[13]

A transfer of assets can be considered fraudulent under US bankruptcy code and state fraudulent transfer laws if the person or company that transferred the assets was insolvent or the transfer resulted in that person or company becoming insolvent.[14]

Failed Capital Commitment

As part of the terms of Prospect’s acquisition of the CharterCARE hospitals in Rhode Island, Prospect committed to making at least $50 million in long term contributions to the hospitals within the first four years of its ownership.[15] This commitment was increased in December 2016 to $61 million and the deadline pushed back to June 2020.[ii]

Based on a March 2020 report from an independent monitor for the Attorney General’s office and a review of Prospect Chartercare’s financial statements, Prospect does not appear to have satisfied its long-term capital commitment.[16]

Our Lady of Fatima Hospital, North Providence

{kind=link}

Monitor for Rhode Island Attorney General only confirmed $29.75 million in capital expenditures

The independent monitor for the Attorney General could only confirm $29.75 million in long-term capital expenditures made by Prospect as of March 2020—less than half of Prospect’s $61 million commitment.[17]

Prospect tried to count operating losses, forgiven management fees and non-cash contributions toward its capital commitment

Some of the “contributions” that Prospect made toward its capital commitment raise questions:

- Prospect attempted to include $14.4 million in operating losses from its physicians’ practices toward its capital expenditures. It is not clear why the physician practices’ operating losses would represent a capital expenditure by Prospect. The Attorney General’s monitor did not confirm those losses as a capital contribution.[18]

- In its financial statements, Prospect CharterCARE notes several cash and non-cash capital contributions made by Prospect Medical Holdings between October 2014 and September 2019 totaling $54.9 million. Only $10.6 million of the total was made of up cash contributions, raising questions about how Prospect could have satisfied its long-term capital commitment.[19]

- The CharterCARE hospitals pay a monthly management fee to Prospect.[20] Prospect counted $20 million in forgiven management fees and $4.7 million in unpaid invoices owed by the hospitals as capital contributions.[21] This is both misleading as Prospect did not actually contribute anything to Prospect CharterCARE by forgiving the management fees, it merely collected less.

Reporting of management fees raise questions about Prospect’s accounting

Much of the management fee liability that Prospect purportedly forgave to satisfy its promised capital commitment in Rhode Island mysteriously appeared on Prospect CharterCARE’s financial statement at the same point Prospect forgave it, raising questions of whether it was a post-facto manipulation of Prospect CharterCARE’s books.[iii]

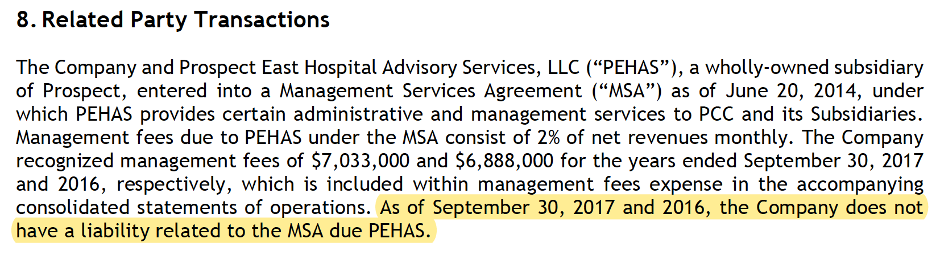

In its 2016-2017 financial statement, Prospect CharterCARE noted that it did not have a liability for management fees as of Sept 20, 2017.[22]

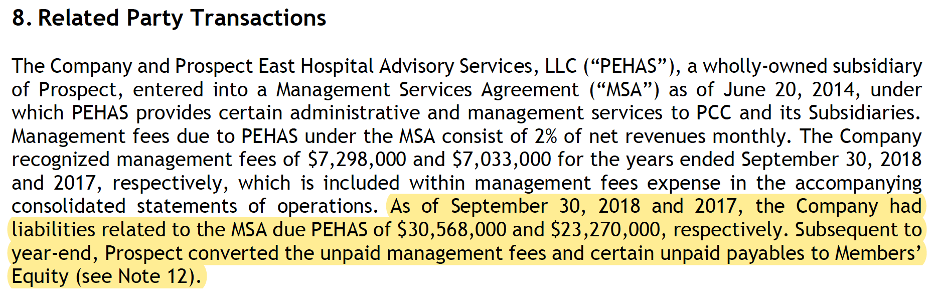

Yet in its 2017-2018 financial statement, Prospect CharterCARE reported a $23.27 million liability for management fees as of Sept 20, 2017, the same date. It was in this financial statement that Prospect disclosed that it had converted unpaid management fees and invoices into equity.[23]

It is striking that Prospect CharterCARE’s management fee liability as of September 2017 was revised from $0 to $23.27 million with no explanation.

Yet as of September 2019, Prospect CharterCARE still reported a year-end management fee liability of $37.96 million, suggesting the management fees were not in fact written off or converted to equity.[24]

Tax Breaks Based on False Promises

The City of Providence and the Town of North Providence provided Prospect with tax exemptions and tax stabilizations based on the understanding that Prospect would invest at least $50 million in capital improvements to the Rhode Island hospitals. In real estate taxes alone, Prospect and its subsidiaries are expected to have saved more than $41.8 million in taxes that would otherwise be due to the City of Providence and Town of North Providence.[25]

Sale-Leaseback Increased Overall Liabilities

In 2019, in an effort to pay down some of the existing $1.1 billion debt it had accrued in part to fund dividends, Prospect sold much of its hospitals’ real estate to health care REIT Medical Properties Trust and leased it back.[26] Prospect and Leonard Green have characterized the sale-leaseback transaction as beneficial to the hospital company,[27] though this is misleading; the sale-leaseback merely replaced debt with lease liabilities and left Prospect with fewer assets.[28]

The terms of Prospect’s new lease are onerous; Prospect is paying more in rent and interest to MPT than it would be paying had it not undertaken the sale-leaseback transaction.[29] Before the transaction, Prospect had $1.35 billion in debt (including $207 million under revolving credit facility). After the transaction, Prospect had $257 million in debt (including $70 million under revolving credit facility) and $1.34 billion in lease liabilities.[30]

Prospect and Leonard Green have praised the deal for allowing Prospect to pay off much of its long-term debt but ignore the fact most of the that debt was a $1.1 billion loan Prospect issued in part to finance a $457 million shareholder dividend.[31]

Valuation and Viability Concerns

The $10 million valuation of Leonard Green’s majority stake in Prospect raises concern, especially given that Leonard Green and Prospect did not utilize a third party to determine the company’s valuation.[32]

In response to a question from the Office of the Attorney General about whether it used external consultants to help value the company, Prospect claimed it “did not require the assistance of external consultants” because “the transacting parties are sophisticated investors in the healthcare industry, including one of the largest private equity firms in the United States.”[33]

Leonard Green’s sale of its majority stake in Prospect is distinctly a non-arms-length transaction: Leonard Green is both the seller and controls the buyer (Prospect) at the time of the transaction.[34] It does not seem appropriate that the firm did not utilize an independent third party to value the company in a non-arms-length transaction, especially given the remarkably low value assigned to the company.

Prospect’s comments on the purchase price are similarly puzzling:

“A primary consideration in the parties’ negotiations was to ensure the long-term viability and success of PMH and its hospitals. With this goal in mind the parties wanted to ensure that PMH will have significant and sufficient resources to meet all of its obligations and to not burden the company with additional debt.”[35]

If Prospect’s ownership was truly concerned about the company’s long-term viability, they would not have drawn at least $457 million dividends from Prospect in the last two years.[36]

Based on Prospect’s FY 2019 financial statement, Leonard Green does not appear to be leaving Prospect with access to “significant and sufficient resources”:[37]

- Prospect’s liabilities ($2.83 billion) dramatically exceeded its assets ($1.86 billion) as of September 2019; and Prospect’s stated assets are somewhat fictitious, as the company still lists its real estate on its balance sheet even through it sold most of it to Medical Properties Trust last year.[38]

- Prospect generated at most $61 million in EBITDA in 2019 (and -$70.7 million in EBITDA when discontinued operations are included).[39]

- By comparison, Prospect pays Medical Properties Trust around $116 million per year in rent.[40] Even before COVID-19, it was not clear how Prospect would be able to pay the rent it owes Medical Properties Trust without incurring additional debt.

- Prospect’s operating activities burned cash in both 2018 and last year – Prospect generated -$71.4 million in cash from operating activities in 2019.[41]

More Failed Commitments

Rhode Island is not the only state where Prospect appears to have broken the promises it made to the communities it serves.

In May 2019, just three years after acquiring East Orange General Hospital (EOGH) in New Jersey, Prospect began looking to sell it. In its application to acquire the hospital, Prospect had made a non-binding commitment to provide in excess of $50 million in operational and capital investments over 5 years after the acquisition.[42] As of the May 2019, when Prospect began trying to sell EOGH, it had reportedly invested just $26 million.[43] As of July 20, Prospect does not appear to have been able to sell the hospital.

East Orange General Hospital, New Jersey

{kind=link}

As part of its acquisition and conversion of the five-hospital Crozer-Keystone Health System in Pennsylvania from non-profit to for-profit, Prospect committed to pay $56.6 million for the establishment of a nonprofit county-wide health foundation, the Crozer-Keystone Community Foundation. Despite its commitment, Prospect initially paid only $32.9 million into the fund. The dispute went to arbitration, and in November 2017 an arbitrator ruled that Prospect still owed the foundation $23.7 million.[44]

Footnotes

[i] In 2019, Prospect paid a $44.4 million shareholder dividend. This dividend was paid to repay a cash infusion made by the owners when Prospect ran out of cash after paying the $457 million dividend in 2018.

[ii] The commitment was increased as a result of Prospect selling Elmhurst Extended Care Facility in Providence, RI. Prospect proposed that the proceeds of the sale be added to the long-term capital commitment in order to comply with conditions in the DOH hospital conversion decision. See Monitoring Report re Prospect CharterCARE, LLC, Mar 20, 2020.

[iii] In its 2016-2017 financial statement, Prospect CharterCARE noted that it did not have a liability for management fees as of Sept 20, 2017. Yet in its 2017-2018 financial statement, Prospect CharterCARE reported a $23.27 million liability for management fees as of Sept 20, 2017, the same date. It was in this financial statement that Prospect disclosed that it had converted unpaid management fees and invoices into equity.

Endnotes

[1]https://pestakeholder.org/wp-content/uploads/2020/05/UPDATE-Leonard-Green-Prospect-Medical-Dividends-PESP-051420.pdf

[2] Prospect CharterCARE Change in Effective Control Application: https://drive.google.com/file/d/1vYdWVfRgKHQ3u_thgjz0qZA7UuPfFWBS/view

[3] Rhode Island Department of Health 2014 decision: https://drive.google.com/file/d/0B9lx-sHDAL9qUE1LWUlIT2pNOGc/view

[4] Letter to Rhode Island Health Services Council from Office of the Attorney General and Department of Health, dated July 14, 2020. http://www.riag.ri.gov/documents/LetterHSCExtensionHCA.pdf

[5] Prospect Medical Holdings Consolidated Financial Statements: 2018-2019, 2017-2018, 2016-2017, 2015-2016

[6] Per the December 2010 Management Services Agreement between Prospect and Leonard Green, Prospect pays Leonard Green an annual management fee of $1 million for “management, consulting and financial planning services” and reimburses Leonard Green for its related expenses up to $50,000 annually. See: Prospect Medical Holdings, Inc. SEC form 10-Q, for the quarterly period March 31, 2011. (pg. 23) https://www.sec.gov/Archives/edgar/data/1063561/000110465911029394/a11-11593_110q.htm

[7] Prospect paid Leonard Green $4.4 million for fees associated with corporate restructuring in 2010. See: Prospect Medical Holdings, Inc. SEC form 10-Q, for the quarterly period March 31, 2011. (https://www.sec.gov/Archives/edgar/data/1063561/000110465911029394/a11-11593_110q.htm) (pg. 23) and Prospect Medical Holdings Company Information Tear Sheet (http://216.117.216.25/pdfs/tearsheet.pdf).

[8] Prospect Medical Holdings Consolidated Financial Statements: 2018-2019, 2017-2018, 2016-2017, 2015-2016

[9] State of Rhode Island Department of the Attorney General, CharterCARE/Prospect Final Decision, pg. 48. http://www.riag.ri.gov/documents/5-16-14AGFinalDecision.pdf

[10] Report of the Committee of the Health Services Council, May 13, 2014. https://drive.google.com/file/d/0B9lx-sHDAL9qRmJPWmd1MXNpbEk/view

[11] Prospect Medical Holdings FY2019 financial statement. https://pestakeholder.org/wp-content/uploads/2020/06/PMH-Financial-Statement-2018-2019.pdf

[12] “Moody’s downgrades Prospect Medical Holdings, Inc.’s CFR to B3; outlook changed to negative,” Moody’s, March 28, 2019. https://www.moodys.com/research/Moodys-downgrades-Prospect-Medical-Holdings-Incs-CFR-to-B3-outlook–PR_397518

[13] Prospect Medical Holdings financial statements, 2017-2019.

[14] 11 U.S. Code § 548. Fraudulent transfers and obligations https://www.law.cornell.edu/uscode/text/11/548 “Delaware Bankruptcy Court

Declines To Dismiss Fraudulent Transfer Suit Filed Seven Years After Challenged Transaction Occurred,” Kramer Levin, Feb 14, 2020. https://www.kramerlevin.com/en/perspectives-search/delaware-bankruptcy-court-declines-to-dismiss-fraudulent-transfer-suit-filed-seven-years-after-challenged-transaction-occurred.html

[15] Prospect CharterCARE Change in Effective Control Decision, May 19, 2014: https://drive.google.com/file/d/0B9lx-sHDAL9qRmJPWmd1MXNpbEk/view

[16] Monitoring Report re Prospect CharterCARE, LLC, Mar 20, 2020.

[17] Monitoring Report re Prospect CharterCARE, LLC, Mar 20, 2020, p. 25.

[18] Monitoring Report re Prospect CharterCARE, LLC, Mar 20, 2020, p.19.

[19] Prospect CharterCARE financial statements 2014-2019.

[20] Management Services Agreement for Prospect CharterCARE hospitals: https://pestakeholder.org/wp-content/uploads/2020/06/Prospect-RI-Management-Services-Agreement.pdf

[21] Prospect CharterCARE, LLC Consolidated Financial Statements as of and for the Years Ended September 30, 2019 and 2018 https://pestakeholder.org/wp-content/uploads/2020/06/Prospect-CharterCARE-financial-statement-2018-2019.pdf (pg. 21).

[22] Prospect CharterCARE, LLC Consolidated Financial Statements as of and for the Years Ended September 30, 2016 and 2017.

[23] Prospect CharterCARE, LLC Consolidated Financial Statements as of and for the Years Ended September 30, 2017 and 2018.

[24] Prospect CharterCARE, LLC Consolidated Financial Statements as of and for the Years Ended September 30, 2018 and 2019.

[25] CCCB v. Lee et al., CA NO. PC-2019-3654; City of Providence Tax Stabilization Agreement: http://providenceri.iqm2.com/Citizens/Detail_LegiFile.aspx?Frame=&MeetingID=10649&MediaPosition=&ID=18850&CssClass=; Ethan Shore, “Agreement ‘stabilizes’ Fatima’s future,” The Valley Breeze, June 3, 2014.

[26]https://www.businesswire.com/news/home/20190715005786/en/Prospect-Receive-1.55-Billion-Investment-Medical-Properties

[27] Tab 23, Prospect’s responses to March 4, 2020 Deficiency Letter sent by the Office of the Health Care Advocate: https://pestakeholder.org/wp-content/uploads/2020/06/C-CIIH23-001096-to-C-CIIH23-001098-Redacted.pdf

[28] Prospect Medical Holdings FY2019 financial statement. https://pestakeholder.org/wp-content/uploads/2020/06/PMH-Financial-Statement-2018-2019.pdf

[29] Prospect Medical Holdings FY2019 financial statement. https://pestakeholder.org/wp-content/uploads/2020/06/PMH-Financial-Statement-2018-2019.pdf

[30] Prospect Medical Holdings FY2019 financial statement. https://pestakeholder.org/wp-content/uploads/2020/06/PMH-Financial-Statement-2018-2019.pdf

[31]https://www.moodys.com/research/Moodys-downgrades-Prospect-Medicals-CFR-to-B2-stable-outlook–PR_378860

[32] Tab 23, Prospect’s responses to March 4, 2020 Deficiency Letter sent by the Office of the Health Care Advocate: https://pestakeholder.org/wp-content/uploads/2020/06/C-CIIH23-001096-to-C-CIIH23-001098-Redacted.pdf

[33] Tab 23, Prospect’s responses to March 4, 2020 Deficiency Letter sent by the Office of the Health Care Advocate: https://pestakeholder.org/wp-content/uploads/2020/06/C-CIIH23-001096-to-C-CIIH23-001098-Redacted.pdf

[34] Prospect CharterCARE Change in Effective Control Application: https://drive.google.com/file/d/1vYdWVfRgKHQ3u_thgjz0qZA7UuPfFWBS/view

[35] Tab 23, Prospect’s responses to March 4, 2020 Deficiency Letter sent by the Office of the Health Care Advocate: https://pestakeholder.org/wp-content/uploads/2020/06/C-CIIH23-001096-to-C-CIIH23-001098-Redacted.pdf

[36]https://pestakeholder.org/wp-content/uploads/2020/05/UPDATE-Leonard-Green-Prospect-Medical-Dividends-PESP-051420.pdf

[37] Prospect Medical Holdings FY2019 financial statement. https://pestakeholder.org/wp-content/uploads/2020/06/PMH-Financial-Statement-2018-2019.pdf

[38] Prospect Medical Holdings FY2019 financial statement.

[39] Ibid.

[40] Ibid.

[41] Ibid.

[42] Ibid.

[43] Anjalee Khemlani, “Prospect Medical seeks to ‘unload’ East Orange General,” ROI-NJ, May 22, 2019. https://www.roi-nj.com/2019/05/22/healthcare/prospect-medical-seeks-to-unload-east-orange-general-to-new-buyer/

[44] Harold Brubaker, “Crozer-Keystone Community Foundation wins arbitrator decision against Prospect Medical,” Philadelphia Inquirer, November 10, 2017. https://www.inquirer.com/philly/business/crozer-keystone-community-foundation-wins-arbitrator-decision-against-prospect-medical-20171110.html